Stock options grants employees the right to buy shares of the company at a set price after a certain period of time. Since there is no cost to the employee, it's essentially free money regardless of when it's exercised. How much the employee makes from the purchase depends is the difference between the "set price", and the market price of the stock.

Typically, companies establish the "set price" of the issued options well below the current market value at the time of issuance so the employee will always be in a net positive position. (...unless the stock price crashes through the floor)

And this is a transfer of wealth from stock holders to the options vester.

If a company is worth 1 million dollars and has 100,000 shares outstanding, those shares are worth 10$, and you give someone 10,000 options at 1$ and they exercise them, the company gets 10,000$ and now has 110,000 shares outstanding. The company is now worth 1,010,000 dollars (the extra 10,000$ increases the company worth by 10,000$), but 110,000 shares means the shares are now worth 9.18$.

Now, in practice, it doesn't cause a change in share price in the instant - the smart investor knows about the options existing, so prices them into the value of the stock

before they are exercised. They act as a (expected share price-1$)*number of options non-cash liability on the books, like a deprecated asset.

But stock options are indeed a transfer of wealth from share holders to the CEO (or other employee). They also happen to be tax-friendly in a few ways, and they produce short-term incentives for the employee to help juke up the stock price.

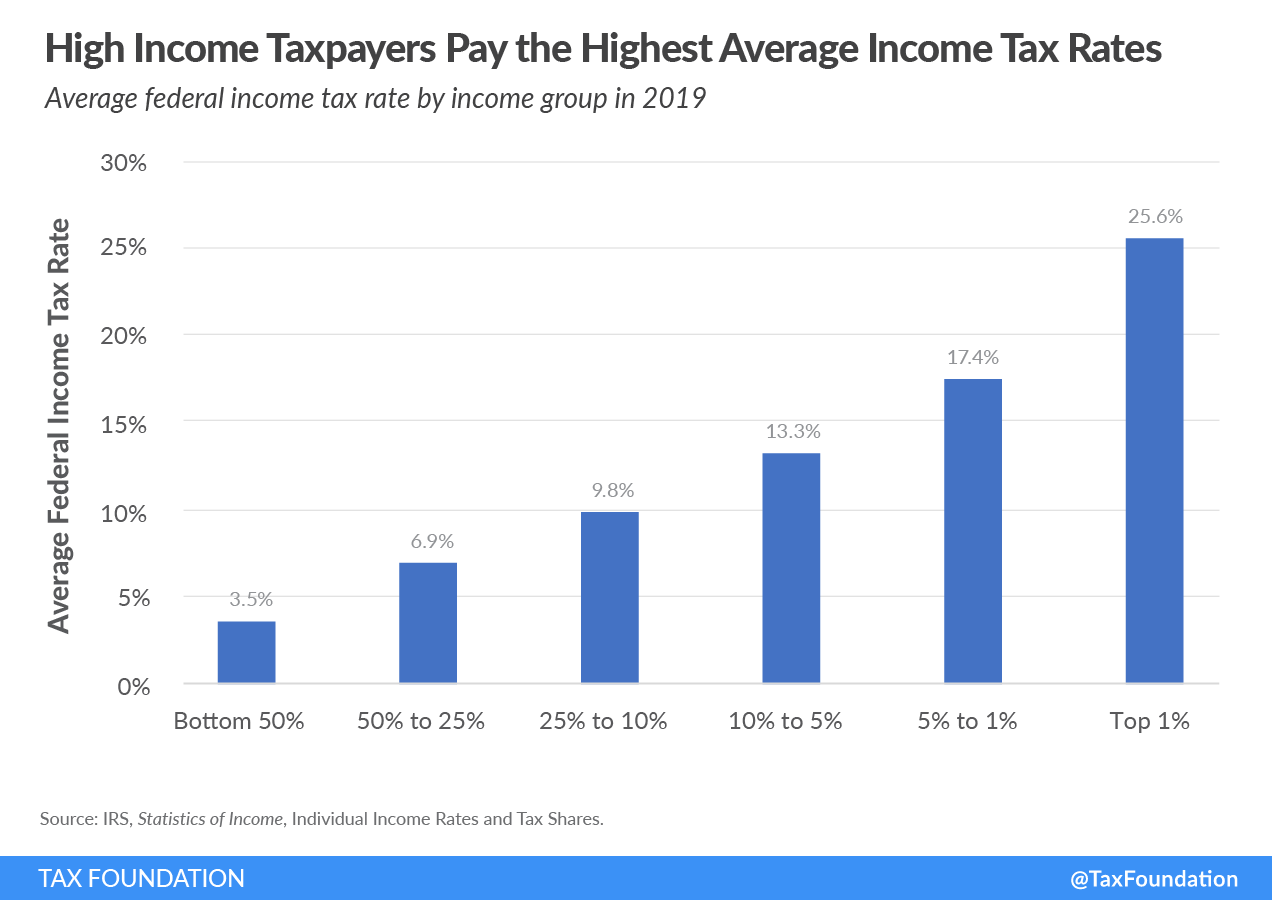

Would say the data doesn't hold with that premise.

This is not to be trusted for a few reasons. Basically, whomever did this picked a way of looking at the data that is

most friendly to their position.

So the first take away should be "never trust anything this organization produces, they are trying to lie to you without saying false statements".

1. Federal income tax is the most progressive tax in the USA. State taxes, especially consumption taxes, are far more regressive.

A 10% sales tax, 100$ a year car registration tax, etc -- all hit the lower income brackets for a larger percentage of their income than the higher income brackets.

2. What we call "Income" is something that the rich avoid. You can gain net worth

without income, and you can even use money to make your life better without it ever counting as income! The poorer you are, the harder it is for your money to avoid being "income".

The simplest example of this is capital gains. If you have an asset that gains in value, you get a lower tax rate, and you only pay taxes on it when you convert it to cash. You can even borrow against its current value and spend that money without paying taxes on its gain in value.

Like, take Bob who earns 100,000$ per year salary. Bob pays income tax of 20% on it (he has a great accountant or something). Bob invests 30,000$ per year and spends 50,000$ per year. His investment grows at 10% per year (!), also taxes at 20%.

After 10 years Bob has spent 500,000$ and has 470,000$ invested and has paid 256,000$ in taxes. Effective tax rate is 26% of what Bob spending+gain in assets.

Alice has a 1 million dollar asset that gain 10% in value every year - also 100,000$ per year gain, but investment not "income". Alice simply borrows 50,000$ spending money against that increasing asset value at 6% interest. Alice pays no taxes until she realizes her capital gains.

After 10 years Alice sells her asset. It is taxed at 10% (half Bob's tax rate, capital gains baby) of its gains. It is worth 2.6 million dollars, of which 1.6 is gains, taxed down to 1.44. The debt is 700,000$, which she pays off. Alice has spend 500,000$ and has 740,000$ surplus (above the initial million) to invest. She has paid 160,000$ in taxes. Effective tax rate of 13% of Alice's spending+gain in assets.

And Alice can do way better than this in the real world; as others have noted, the total tax rate of the top 1% tends to be tiny.

What more, suppose consumption taxes are 10%. This is 50,000$ to both of them, but a larger percentage of Bob's money than Alice's.

This is a situation where both are normally equally wealthy. If we now go and boost Alice's investment income by 10x, her consumption of things we tax doesn't go up 10x - food, gas, consumer goods. Her consumption of things we don't tax the same way - donations to attend galas, buying politicians, donations to schools to get her kids in, country club "foundation" donations, real estate, companies, etc - go up.

")